简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Less Dovish Fed May Boost USD/SGD as More Dovish BSP Lifts USD/PHP

Abstract:The US Dollar may rise on a Fed that is not quite as dovish as markets expect, sending USD/SGD higher as ASEAN currencies depreciate. USD/PHP

ASEAN Fundamental Outlook

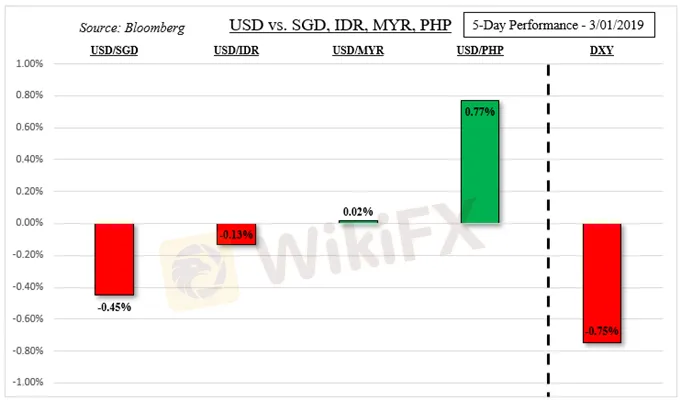

US Dollar depreciation boosted most ASEAN currencie

The Philippine Peso may weaken on BSP rate decisio

Less-dovish Fed may send USD/MYR and USD/SGD u

Trade all the major global economic data live and interactive at the DailyFX Webinars. Wed love to have you along.

US Dollar and ASEAN FX Reca

The US Dollar had its worst week since August as DXY fell about 0.80%. Weakness was partially owed to a broadly stronger British Pound, which rallied the most when the UK Parliament voted to reject a ‘no-deal’ Brexit in any circumstances. Meanwhile, the S&P 500 trimmed its losses from the previous week, sapping demand for safe havens and the highly liquid Greenback.

As such, this allowed for some ASEAN currencies to gain ground against the US Dollar. Most notably was USD/SGD which tends to have a close positive correlation to the Greenback. The same could not be said for the Philippine Peso, which continues to selloff after the central banks new governor brought with him dovish rhetoric. Meanwhile, the Indonesian Rupiah trimmed losses after local exports contracted more than expected.

Domestic ASEAN FX Economic Events and Risk

The week ahead contains multiple central bank interest rate announcements, both regionally and externally. Beginning with the former, the Philippine Peso may weaken on the Bangko Sentral ng Pilipinas (BSP) monetary policy decision. While rates are anticipated to be left unchanged, the central bank‘s new governor, Benjamin Diokno, may allude to easing in the future and confirm hopes to cut banks’ reserve requirement ratios.

Philippine inflation has significantly slowed from a peak of 6.7% y/y towards the end of last year to now 3.8% in February. This is within the BSPs target range and if it remains there, perhaps reaching the lower boundary, it may open the door to a cut down the road. Falling oil prices (towards the end of last year) have played an important part as the commodity is a key import.

Meanwhile, the USD/IDR looks to the Bank of Indonesia where rates are also seen to be left on hold. The Indonesian Rupiah has been weakening versus the US Dollar since February as the central bank remained on hold. Watch for what they have to say about the fundamental value of the Rupiah. The central bank has been intervening as they believe the currency to be undervalued. More of the same rhetoric may boost IDR.

External ASEAN FX Event Risk

All eyes will be on the Federal Reserve this week with Fed funds futures pricing in a 32.3% chance of a cut by the end of this year. This means markets are anticipating the central bank to downgrade their view on interest rate hikes this year. Having said that, leaving the door open to just one increase is still more hawkish than what markets anticipate.

As such, risks for the US Dollar are arguably tilted to the upside as it would take a surprisingly cautious announcement to fuel dovish bets. If the Greenback rallies, then USD/SGD is likely to follow higher. Meanwhile, technical warnings hint USD/MYR may rise in the medium-term.

For updates on the Philippine Peso, Malaysian Ringgit, Singapore Dollar and Indonesian Rupiah, you may follow me on Twitter here @ddubrovskyFX for more timely updates. I will also be updating the technical forecast later this week.

FX Trading Resource

Just getting started? See our beginners guide for FX trader

Having trouble with your strategy? Heres the #1 mistake that traders make

--- Written by Daniel Dubrovsky, Junior Currency Analyst for DailyFX.com

To contact Daniel, use the comments section below or @ddubrovskyFX on Twitter

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

KVB Market Analysis | 30 August: JPY Strengthens Against USD Amid Strong Q2 GDP and BoJ Rate Hike Speculation

The Japanese Yen (JPY) strengthened against the US Dollar (USD) on Thursday, boosted by stronger-than-expected Q2 GDP growth in Japan, raising hopes for a BoJ rate hike. Despite this, the USD/JPY pair found support from higher US Treasury yields, though gains may be capped by expectations of a Fed rate cut in September.

KVB Market Analysis | 28 August: Yen Strengthens on BoJ Rate Hike Hints; USD/JPY Faces Uncertainty

The Japanese Yen rose 0.7% against the US Dollar after BoJ Governor Kazuo Ueda hinted at potential rate hikes. This coincided with a recovery in Asian markets, aided by stronger Chinese stocks. With the July FOMC minutes already pointing to a September rate cut, the US Dollar might edge higher into the weekend.

KVB Market Analysis | 27 August: AUD/USD Holds Below Seven-Month High Amid Divergent Central Bank Policies

The Australian Dollar (AUD) traded sideways against the US Dollar (USD) on Tuesday, staying just below the seven-month high of 0.6798 reached on Monday. The downside for the AUD/USD pair is expected to be limited due to differing policy outlooks between the Reserve Bank of Australia (RBA) and the US Federal Reserve. The RBA Minutes indicated that a rate cut is unlikely soon, and Governor Michele Bullock affirmed the central bank's readiness to raise rates again if necessary to combat inflation.

KVB Market Analysis | 23 August: JPY Gains Ground Against USD as BoJ Signals Possible Rate Hike

JPY strengthened against the USD, pushing USD/JPY near 145.00, driven by strong inflation data and BoJ rate hike expectations. Japan's strong Q2 GDP growth added support. However, USD gains may be limited by expectations of a Fed rate cut in September.

WikiFX Broker

Latest News

RM750 Million Lost to Investment Scams in Just Six Months

WikiFX

WikiFX5 things to know before the Thursday open: Meme stock revival, Trump's Fed visit, Uber's gender feature

WikiFXWhy Octa Is the Ideal Broker for MetaTrader 4 & 5 Users

WikiFXCNBC's Inside India newsletter: Leaving, but not letting go — India's wealthy move abroad, but stay invested

WikiFXMoncler raises prices on tariffs, may postpone store openings if downturn worsens

WikiFXTitan FX Adds WhatsApp and Telegram for Enhanced Support

WikiFXNestle flags further potential price hikes as tariffs, commodities weigh on margins

WikiFXStop Level Forex: How Does it Help Traders Prevail When Losses Mount?

WikiFXeToro Launches Spot-Quoted Futures Trading in Spain

WikiFXTitan FX Introduces Redesigned Client Cabinet for Enhanced Usability

WikiFXCurrency Calculator