简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

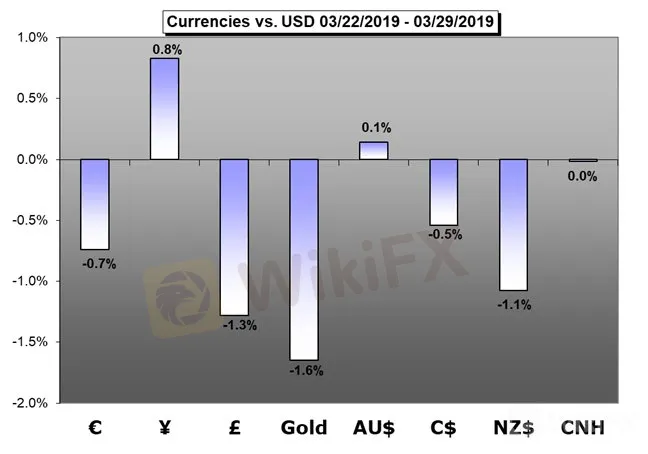

Weekly Fundamental Forecast: Recession and Brexit Worries face QE and Trade Talk Hopes

Abstract:Risk trends still have the fundamental winds to their back, and speculatively-dependent assets such as equities and commodities have benefited. Yet, the balance of power and themes into the second quarter looks far less convincing than how markets have performed. Trying to untangle trade wars and unequipped central banks ramping

Crude Oil Forecast – Crude Oil May be Overextended, But Watch Out For Trade Headlines

Crude oil prices remain supported by supply cuts and trade deal hopes even as the economic data have proven disappointing. That support could wane a little this week

British Pound Forecast – GBP/USD Rate Threatens Bull Trend Ahead of Brexit Deadline

The British Pound may face a more bearish fate ahead of the Brexit deadline in April as the GBP/USD exchange rate threatens the upward trend from late last year

US Dollar Forecast – US Dollar May Rise as Sentiment Succumbs to Potent Headwinds

The US Dollar may rise, spurned on by haven-seeking capital flows as risk appetite finally succumbs to a broad assortment of potent headwinds.

Gold Forecast – Gold Price Outlook Bearish as USD May Rise on Soft Econ Data, RBA

Gold prices could be weighed down if the US Dollar rises in risk aversion on soft economic data. Other hazards for the precious metal include a more dovish RBA and Brexit updates

Equities Forecast – Dow Jones, FTSE 100, DAX 30 and ASX 200 Fundamental Forecast

The Dow Jones will look to a slew of economic data out of the United States while the FTSE and DAX await Brexit clarification. Elsewhere, the ASX 200 awaits a rate decision from the RBA.

See what live coverage is scheduled to cover key event risk for the FX and capital markets on the DailyFX Webinar Calendar.

See how retail traders are positioning in the majors using the IG Client Sentiment readings on the sentiment page.

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

Read more

What is Forex Trading and How Does It Work? (A Complete 2025 Guide for Beginners)

Your First Step Welcome to the foreign exchange market, the largest and most l

Decoding Excellence: The Top 10 Forex Brokers in the World for 2025

Meet the World‘s Elite: An Overview of the Top 10 Forex Brokers These brokers a

Unlock 2025 Forex Trading: What Is Forex Trading and How Does It Work Today?

Introduction: Understanding the World‘s Largest Financial Market Forex trading

Upbeat U.S. GDP Spurs Dollar Strength

The U.S. GDP released yesterday surpassed market expectations, which has tempered some speculation about a Fed rate cut and spurs dollar's strength.

WikiFX Broker

Latest News

What WikiFX Found When It Looked Into Vestrado

WikiFX

WikiFXIs the Forex Bonus a Genuine Perk or Just a Gimmick?

WikiFXeToro Joins Hands with Premiership Women’s Rugby

WikiFXOctaFX Was Fined $37,000 for Operating Without a License

WikiFXHantec Financial: A Closer Look at Its Licenses

WikiFXSaxo Bank Fined €1 Million by AMF Over Compliance Failures During IT Migration

WikiFXCySEC Flags Two Unlicensed Investment Platforms: greymax.net and finotivefunding.com

WikiFXHantec Markets Appoints New Executives for Growth in Dubai

WikiFXOlymptrade Under Fire – Fraud Allegations and Investor Outrage

WikiFXGoPro, Krispy Kreme join the meme party as Wall Street speculation ramps up

WikiFXCurrency Calculator